The Random Forest analysis techniques was used to improve prediction on the German Credit Dataset.

The dataset is found:

url="http://freakonometrics.free.fr/german_credit.csv"

credit=read.csv(url, header = TRUE, sep = ",")str(credit)## 'data.frame': 1000 obs. of 21 variables:

## $ Creditability : int 1 1 1 1 1 1 1 1 1 1 ...

## $ Account.Balance : int 1 1 2 1 1 1 1 1 4 2 ...

## $ Duration.of.Credit..month. : int 18 9 12 12 12 10 8 6 18 24 ...

## $ Payment.Status.of.Previous.Credit: int 4 4 2 4 4 4 4 4 4 2 ...

## $ Purpose : int 2 0 9 0 0 0 0 0 3 3 ...

## $ Credit.Amount : int 1049 2799 841 2122 2171 2241 3398 1361 1098 3758 ...

## $ Value.Savings.Stocks : int 1 1 2 1 1 1 1 1 1 3 ...

## $ Length.of.current.employment : int 2 3 4 3 3 2 4 2 1 1 ...

## $ Instalment.per.cent : int 4 2 2 3 4 1 1 2 4 1 ...

## $ Sex...Marital.Status : int 2 3 2 3 3 3 3 3 2 2 ...

## $ Guarantors : int 1 1 1 1 1 1 1 1 1 1 ...

## $ Duration.in.Current.address : int 4 2 4 2 4 3 4 4 4 4 ...

## $ Most.valuable.available.asset : int 2 1 1 1 2 1 1 1 3 4 ...

## $ Age..years. : int 21 36 23 39 38 48 39 40 65 23 ...

## $ Concurrent.Credits : int 3 3 3 3 1 3 3 3 3 3 ...

## $ Type.of.apartment : int 1 1 1 1 2 1 2 2 2 1 ...

## $ No.of.Credits.at.this.Bank : int 1 2 1 2 2 2 2 1 2 1 ...

## $ Occupation : int 3 3 2 2 2 2 2 2 1 1 ...

## $ No.of.dependents : int 1 2 1 2 1 2 1 2 1 1 ...

## $ Telephone : int 1 1 1 1 1 1 1 1 1 1 ...

## $ Foreign.Worker : int 1 1 1 2 2 2 2 2 1 1 ...convert categorical variables as factors,

F=c(1,2,4,5,7,8,9,10,11,12,13,15,16,17,18,19,20)

for(i in F) credit[,i]=as.factor(credit[,i])create our training/calibration and validation/testing datasets, with proportion 1/3-2/3

i_test=sample(1:nrow(credit),size=333)

i_calibration=(1:nrow(credit))[-i_test]LogisticModel <- glm(Creditability ~ Account.Balance + Payment.Status.of.Previous.Credit + Purpose +

Length.of.current.employment +

Sex...Marital.Status, family=binomial,

data = credit[i_calibration,])fitLog <- predict(LogisticModel,type="response", newdata=credit[i_test,])library(ROCR)## Warning: package 'ROCR' was built under R version 3.3.3## Loading required package: gplots##

## Attaching package: 'gplots'## The following object is masked from 'package:stats':

##

## lowess## Loading required package: methodspred = prediction( fitLog, credit$Creditability[i_test])

perf <- performance(pred, "tpr", "fpr")

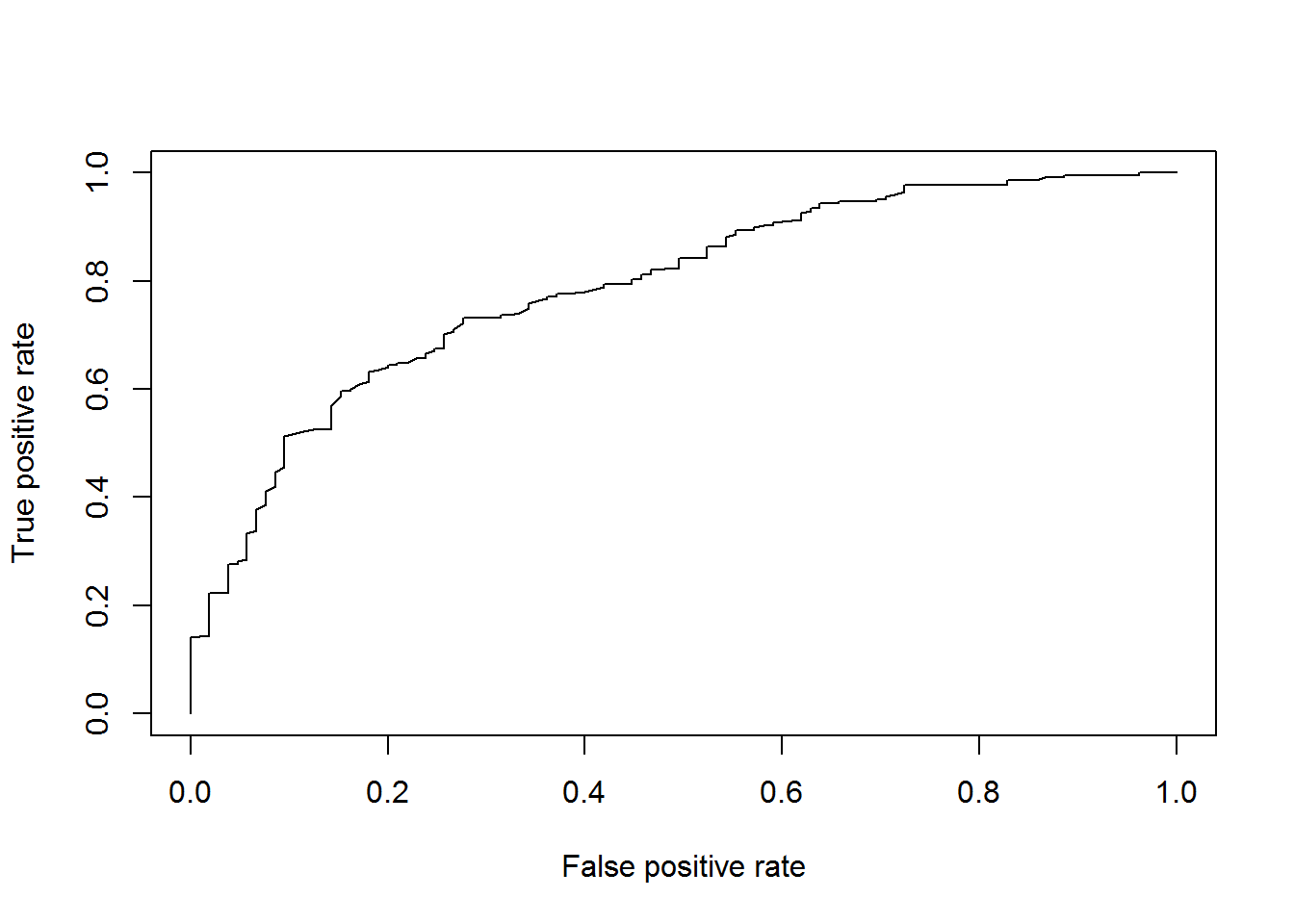

plot(perf)

AUCLog1=performance(pred, measure = "auc")@y.values[[1]]

cat("AUC: ",AUCLog1,"n")## AUC: 0.7340226 nAlternative is to consider a logistic regression on all explanatory variables

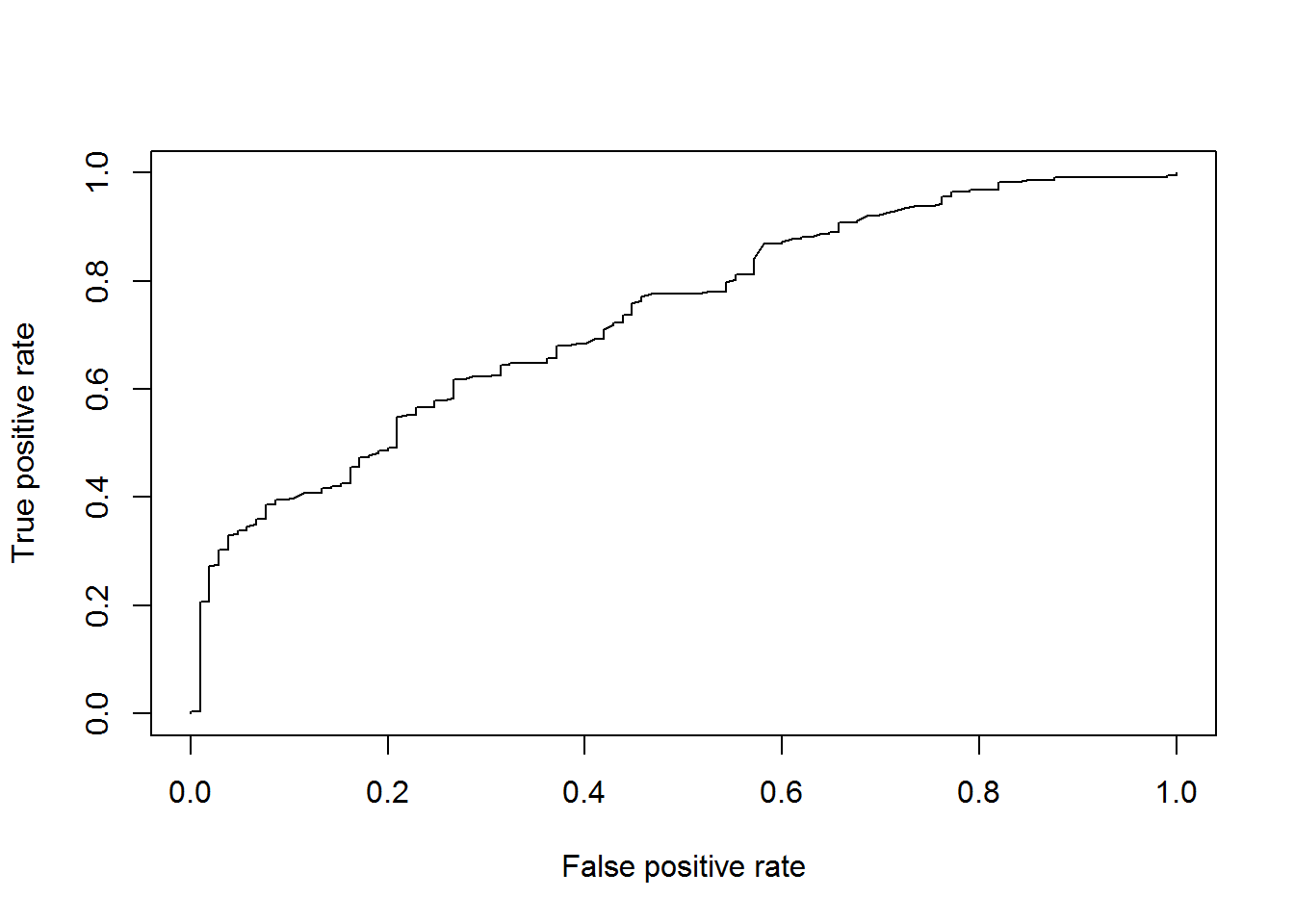

LogisticModel <- glm(Creditability ~ ., family=binomial, data = credit[i_calibration,])

fitLog <- predict(LogisticModel,type="response",newdata=credit[i_test,])

pred = prediction( fitLog, credit$Creditability[i_test])

perf <- performance(pred, "tpr", "fpr")

plot(perf)

AUCLog2=performance(pred, measure = "auc")@y.values[[1]]

cat("AUC: ",AUCLog2,"n")## AUC: 0.7532581 nRegression tree method

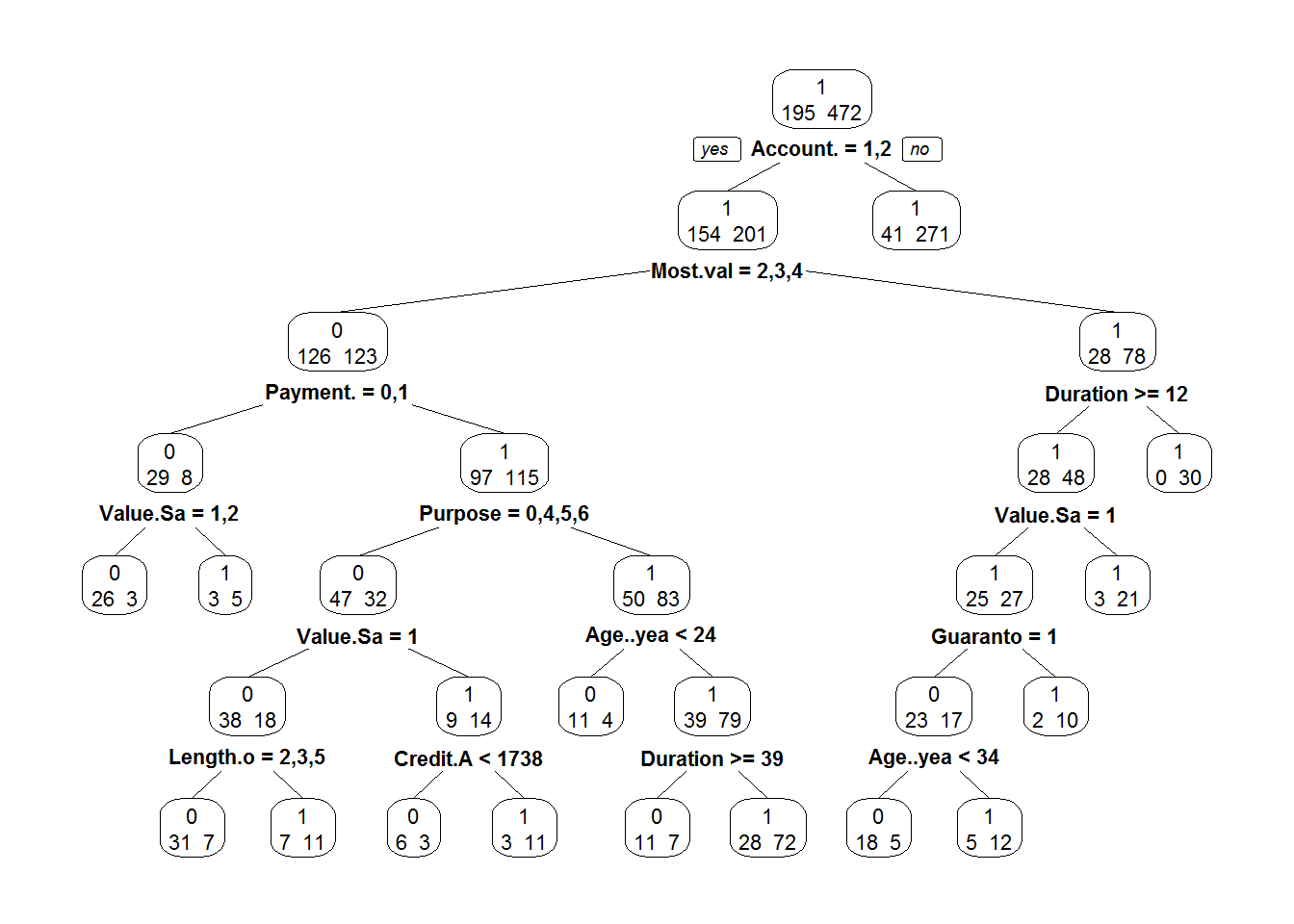

library(rpart)

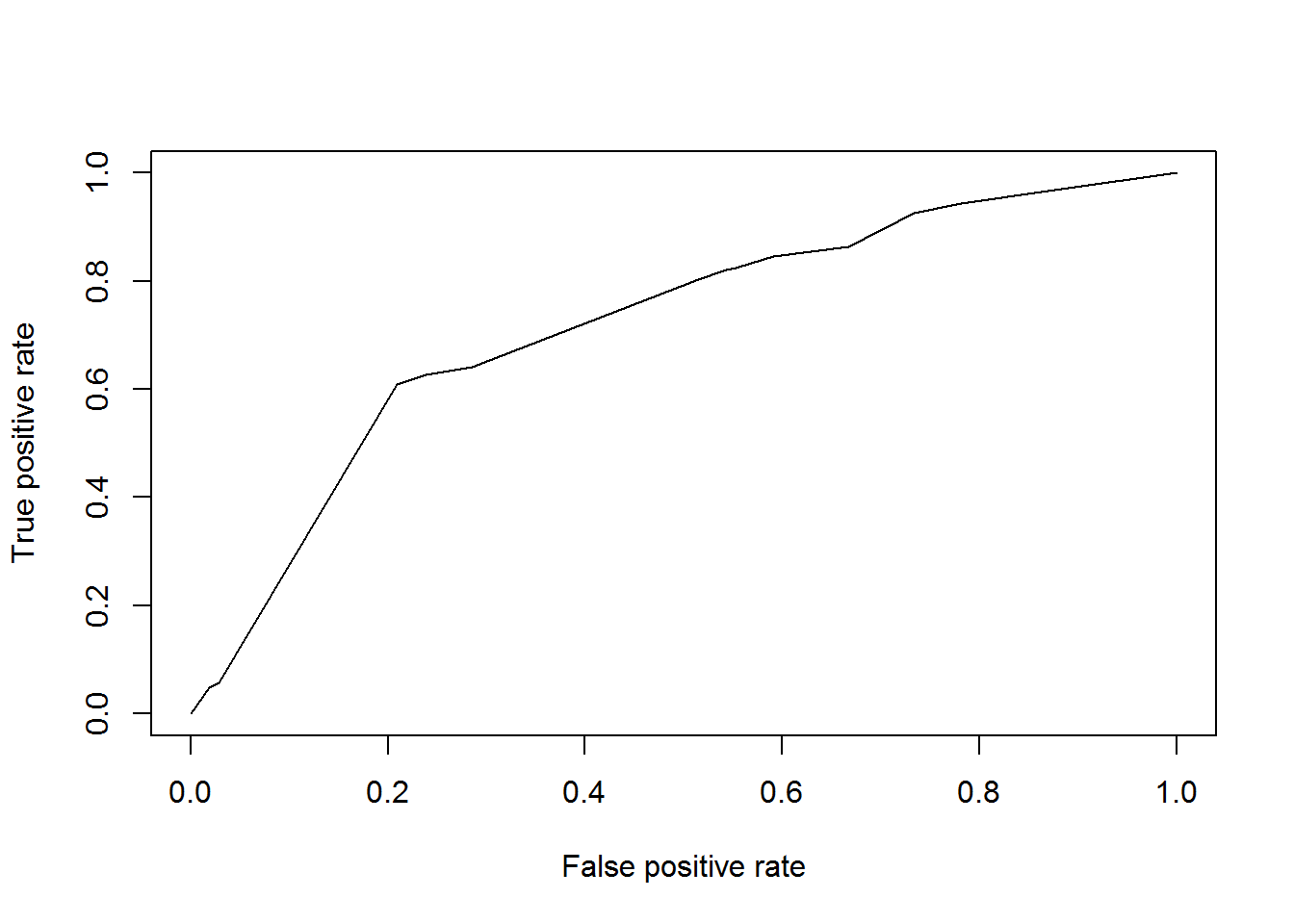

ArbreModel <- rpart(Creditability ~ ., data = credit[i_calibration,])library(rpart.plot)## Warning: package 'rpart.plot' was built under R version 3.3.3prp(ArbreModel,type=2,extra=1)

fitArbre <- predict(ArbreModel, newdata=credit[i_test,],type="prob")[,2]

pred = prediction( fitArbre, credit$Creditability[i_test])

perf <- performance(pred, "tpr", "fpr")

plot(perf)

AUCArbre=performance(pred, measure = "auc")@y.values[[1]]

cat("AUC: ",AUCArbre,"n")## AUC: 0.719152 nRandom Forest analysis

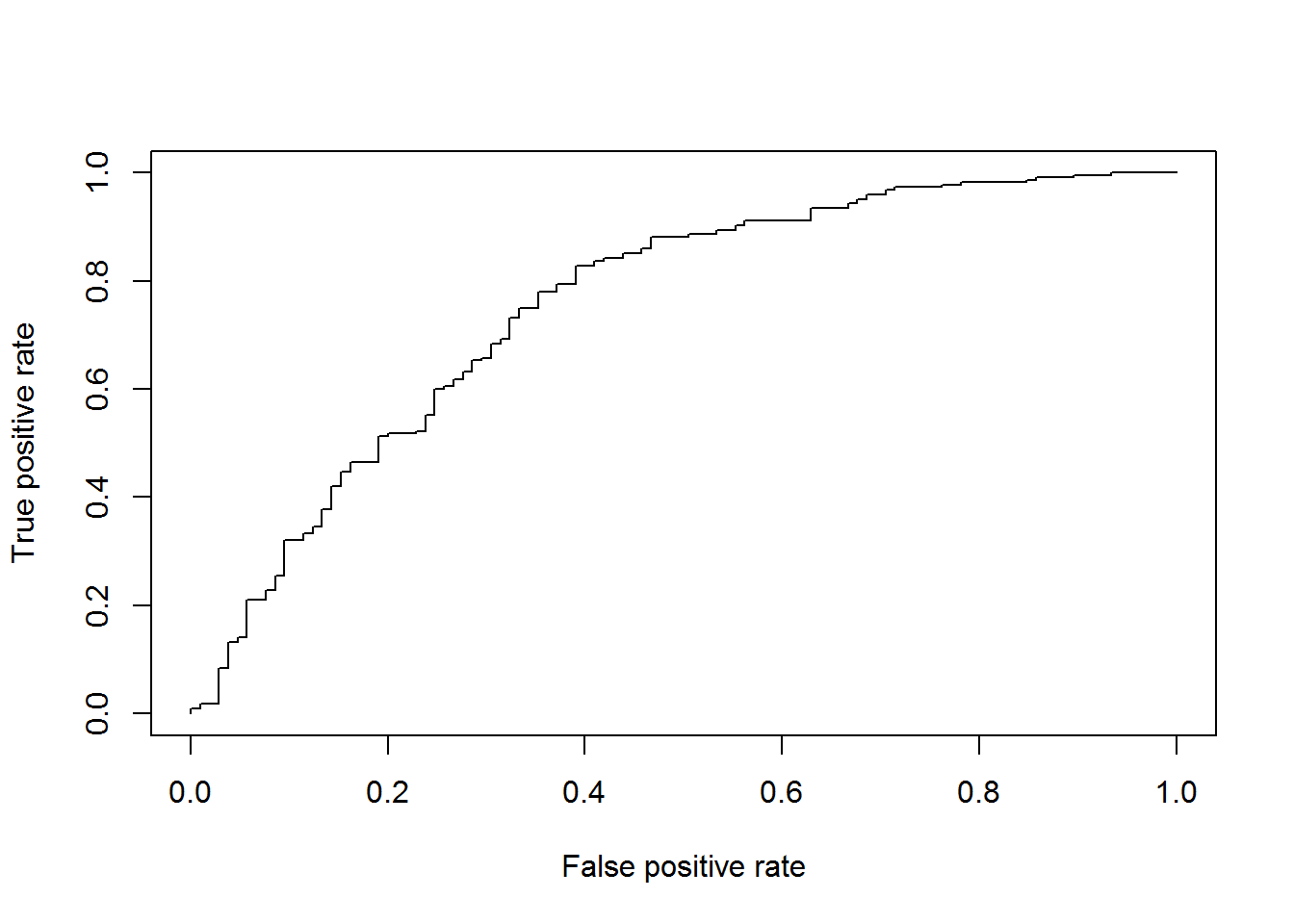

library(randomForest)## Warning: package 'randomForest' was built under R version 3.3.3## randomForest 4.6-12## Type rfNews() to see new features/changes/bug fixes.RF <- randomForest(Creditability ~ .,data = credit[i_calibration,])

fitForet <- predict(RF,newdata=credit[i_test,],type="prob")[,2]

pred = prediction( fitForet, credit$Creditability[i_test])

perf <- performance(pred, "tpr", "fpr")

plot(perf)

AUCRF=performance(pred, measure = "auc")@y.values[[1]]

cat("AUC: ",AUCRF,"n")## AUC: 0.7892439 n

Share this post

Twitter

Google+

Facebook

Reddit

LinkedIn

StumbleUpon

Email